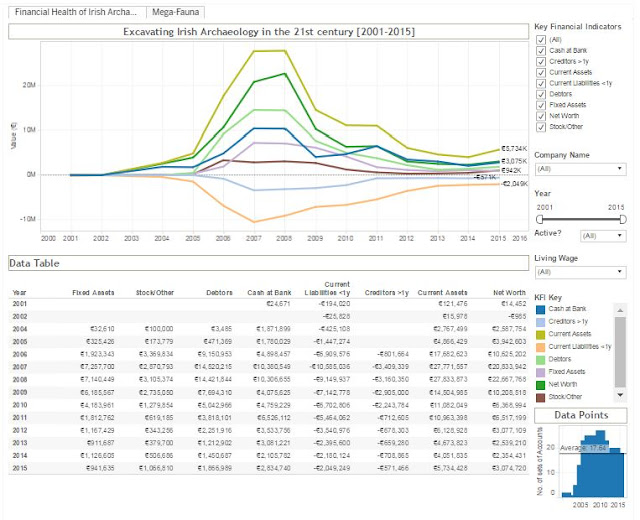

Screenshot of the Tableau Dashboard. Available [ here ] and at the end of this post Background Archaeologists are supposed to be rather good at digging … out in the field it’s quite a bit of what we do. When I left field archaeology in 2011 it was, I suppose, inevitable that I would find something else to delve and dig into. One of the topics that has engaged my attention in recent years is the reconstruction of the financial histories of individual archaeological consultancies to create an impression of the sector as a whole, based on a few publicly available ‘Key Financial Indicators’. The process started with an examination of Northern Ireland’s four archaeological consultancies for the period from 2007-2013 [ here ] and, while imperfect, was sufficient to plot much of the post-2008 collapse of the industry, even if the 2013 data was only for a single company. A second post [ here ] updated the dataset with the 2013 financial details of two further companies. My original p...