Another turn round the plughole? Commercial Archaeology in Northern Ireland in 2014

[If you like what I write, please consider throwing something in the Tip Jar on the right of the page. Alternatively, using the site portals for shopping on either Amazon.com or Amazon.co.uk brings in some advertising revenue and costs you nothing]

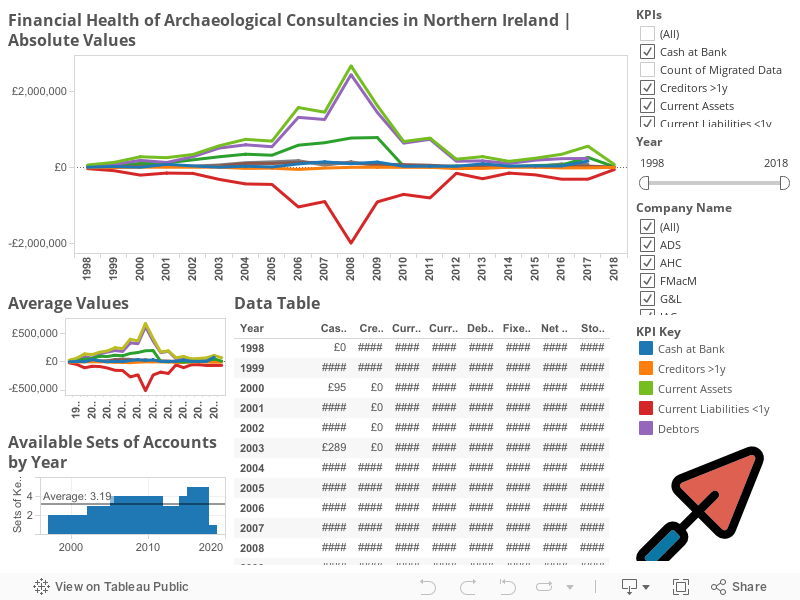

As we rapidly plunge towards the end of another year, many people’s minds turn to Yule festivities, gifting, feasting, quaffing and all the joys that the Winter Solstice has to offer. For myself, I find my mind turning to the financial health of the archaeological sector in Northern Ireland, because that’s just how I roll. In what is becoming something of a year-end tradition, I’ve been looking at a number of Key Financials for the four main archaeological consultancies in Northern Ireland. Previous posts have analysed the period from 2011-2012 and 2013. A recent post on the commercial archaeological sector in the Republic of Ireland made use of a Tableau dashboard to display the data and allow a degree of user interactivity beyond the traditional static images of graphs and tables [here]. I have attempted to do the same with the Northern Irish data and the dashboard is available at the end of this post, or directly on the Tableau Public server: here. For anyone not familiar with how this dashboard works, I would recommend taking a look at my notes on the Republic of Ireland one [here] as they are largely identical. As before, I have chosen to only refer to the individual companies by their year of incorporation, but (based on the legal advice given to me) I have provided an Appendix where the reader can link directly to the records I have based my calculations on and the real names of the companies involved [here].

As we rapidly plunge towards the end of another year, many people’s minds turn to Yule festivities, gifting, feasting, quaffing and all the joys that the Winter Solstice has to offer. For myself, I find my mind turning to the financial health of the archaeological sector in Northern Ireland, because that’s just how I roll. In what is becoming something of a year-end tradition, I’ve been looking at a number of Key Financials for the four main archaeological consultancies in Northern Ireland. Previous posts have analysed the period from 2011-2012 and 2013. A recent post on the commercial archaeological sector in the Republic of Ireland made use of a Tableau dashboard to display the data and allow a degree of user interactivity beyond the traditional static images of graphs and tables [here]. I have attempted to do the same with the Northern Irish data and the dashboard is available at the end of this post, or directly on the Tableau Public server: here. For anyone not familiar with how this dashboard works, I would recommend taking a look at my notes on the Republic of Ireland one [here] as they are largely identical. As before, I have chosen to only refer to the individual companies by their year of incorporation, but (based on the legal advice given to me) I have provided an Appendix where the reader can link directly to the records I have based my calculations on and the real names of the companies involved [here].

|

| Screenshot of the completed vizualisation |

|

| 1997 Co. 2008-2014 |

|

| 2002 Co. 2008-2014 |

|

| 2005 Co. 2008-2014 |

|

| Summed financial values for all NI Companies 2007-2014 |

With the exception of

the Current Liabilities data, the trend lines here are all on the way down. Viewing

it in the most optimistic light would only allow me to say that the Cash at

Bank trend is flat. This is nothing to celebrate for these companies. The

results for 2014 may be marginally better than those for the previous year, but

the sector has collapsed and shows no real signs of regeneration. There is no

evidence of any green

shoots of recovery. The best picture that can be drawn here is one of

continued stagnation, if not slow degeneration and destruction.

As I’ve always tried to

make clear, my posts regarding the financial health of these enterprises are

not ends in themselves, but a means of examining the fragility of the

commercial archaeological sector. Most importantly, this data illustrates the vulnerability

of the site archives that these companies hold. Should one of these groups

finally slip over the edge and be forced to wind up their operations, there is

a huge potential for a large number of important but unpublished archives to be permanently

lost to scholarship. The last

time I wrote on this subject, I noted that there was no movement from the

NIEA to address this continuing crisis. As far as I can ascertain, nothing has

changed on this front. However, in October 2014, I thought that a potential

answer may lie in the high quality work of the Centre

for Archaeological Fieldwork at QUB. However, in 2015 it lost its funding

and at the time of writing operates in a much reduced capacity.

Despite everything, it

would appear that 2014 has been the bleakest year on record for commercial

sector archaeology in Northern Ireland. In October of last year I ended my post

with this:

“In the meantime we can only wait for the 2014 figures and

see if genuine recovery materialises or the slow circling of the plughole

continues.”

Well, no recovery

materialised and the slow circling continues … I wonder what developments 2015

will bring?

Notes

For the best viewing

experience of the Tableau dashboard, I would recommend going to Full Screen

mode (F11) … there will be less scrolling needed!

Comments

Post a Comment